The diamond industry was mixed in March as the Middle East war added new pressures.

The market remained split between small and large goods. Trading in Israel and Dubai froze amid Iranian missile strikes following the start of the conflict on February 28.

US tariffs on Indian goods remained a worry for dealers, despite having fallen to 10% in February.

Polished diamonds of 2 carats and larger were in demand and in short supply, especially in long fancy shapes. Large New York wholesalers saw steady orders from retailers.

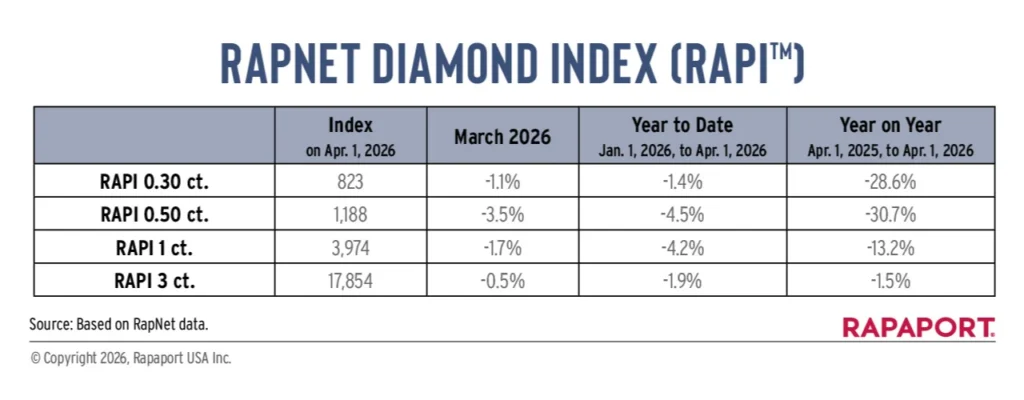

The RapNet Diamond Index (RAPI™) for 1-carat diamonds, which tracks round, D to H, IF to VS2 goods, fell 1.7% in March. The RAPI for 0.30- and 0.50-carat diamonds declined 1.1% and 3.5%, respectively. The 3-carat index dropped 0.5%.

The Rapaport Price List went down in round diamonds of up to 1.99 carats and pears of up to 0.99 carats on March 20. Rapaport CEO Dan Mano’s public message following the changes helped the market react in a measured way.

Rough tender houses relocated their sales because of the Dubai situation. Concerns arose about Indian manufacturers’ access to goods. Roughs of 5 carats and larger remained sought-after amid tight supply, with reports of price increases at De Beers’ March sight.

De Beers removed 20 to 25 sightholders from its 69-strong client list for the new contract period that begins 1 July, seeking greater efficiency. The move also reflected an overall reduction in rough supply and demand.

Signet Jewellers reported sales of US$6.81 billion for the fiscal year that ended 31 January, a 1.6% increase from the previous year. The company is closing its James Allen e-commerce site and absorbing the brand into Blue Nile, which will now focus mostly on natural diamonds.The RAPI is the average asking price, in hundreds of dollars per carat, of the 10% lowest-priced round diamonds in each of the top 25 quality categories (D-H, IF-VS2, GIA-graded, RapSpec-A3 and better) offered for sale on RapNet. –www.rapaport.com.